The statements made and opinions expressed in this publication are solely the responsibility of the author(s) and do not necessarily reflect the opinions of the Security in Context network, its partner organizations, or its funders.

By Celio Hiratuka

Affiliation

Professor at Institute of Economics, Universidade Estadual de Campinas (UNICAMP)

Coordinator of the Brazil China Study Group at UNICAMP and Researcher at the Center for Technology and Industrial Economics, IE-UNICAMP

This paper was prepared for the online conference, The China Effect: Rethinking Development in Latin America and the Caribbean, that took place on December 3, 2025, and organized by the University of Oklahoma Center for Peace and Development, the Security in Context Network (SiC), and the Center for Chinese Mexican Studies (Cechimex) at the School of Economics at the National Autonomous University of Mexico (UNAM).

Abstract: This paper examines the rapid transformation of Brazil-China economic relations over the past twenty-five years and evaluates their implications for Brazilian development. China’s emergence as their leading trading partner has reshaped Brazil’s external sector, displacing traditional partners such as the United States, the European Union, and Argentina.

The paper also analyzes the evolution of Chinese foreign direct investment in Brazil. Although still smaller than US investment, Chinese FDI has expanded significantly and shifted from natural resources and electricity toward manufacturing and high‑technology sectors, including electric vehicles and digital infrastructure. This shift reflects China’s broader strategy of fostering innovation and “new quality productive forces.”

The article concludes that Brazil faces a complex scenario shaped by intensifying US-China rivalry. Navigating this environment requires a development strategy capable of leveraging opportunities while addressing structural vulnerabilities in industry, technology, and sustainability.

Citation: Hiratuka, Celio, 2026. “Economic Relations Between Brazil and China: Challenges for Development in a Scenario of Transformations in the Global Order.,” Security in Context Research Paper 26-01. April 2026, Security in Context.

Introduction

Over the past twenty-five years, economic relations between Brazil and China have undergone a profound transformation, becoming more internationally relevant. From a minor exporter and investor in the early 2000s, China has become Brazil's main trading partner and, at the same time, one of its principal investors.

In this process, China began to compete for an increasingly significant share with Brazil's former commercial partners and traditional investors. The United States, the European Union, and Argentina suffered notable losses in market share, both as sources and destinations of Brazilian trade flows. In terms of Foreign Direct Investments (FDI) in Brazil, the process of China’s growing importance is more recent but increasingly relevant.

However, it is important to recognize the significant changes taking place in the global economy, where there is a clear rupture in the international order. The United States is deliberately dismantling the multilateral framework it has led since the postwar period and positioning China as the power to be contained. This necessarily brings into discussion how and to what extent China's rise is affecting the United States’ position in the region (Dussel Peters, 2025; Heines, 2025). Particularly in its new foreign policy, the US explicitly reaffirms its “prominence” in the Western Hemisphere, reviving the Monroe Doctrine to contain China’s influence, with references to combating drug trafficking, reducing illegal immigration, and pursuing US’ reindustrialization through commercial pressures on regional economies (Costa and Ricúpero, 2025).

This paper provides a brief analysis of the evolution of Brazil’s economic relations with China. It examines the economic debate over these relations on Brazilian economic development. The paper also presents a comparative analysis of Brazil’s trade and investment flows with other regions, focusing particularly on the United States. On one hand, it highlights the reduction in the importance of the United States as Brazil’s commercial partner; on the other, it underscores the still predominant role of US companies in the Brazilian economic system through their multinational operations.

Thus, the paper contributes to the debate on the structural impact of China’s rise on Brazil, incorporating the new conditions associated with increased rivalry between China and the United States and the US effort to reaffirm its hegemonic position in Latin America. The article is structured into three sections, in addition to this introduction. Section 2 analyzes the profile of Brazil’s trade with China, also highlighting how other traditional partners, such as the United States, the European Union, and Argentina, have lost ground both as destinations for Brazilian exports and as sources of imports. Section 3 examines Chinese investments in Brazil. Although flows have increased in recent years, the section emphasizes how US multinationals still play a significant role in the Brazilian productive system. Nevertheless, China’s growing presence is likely to become the new battleground in competition with other regions. Section 4 concludes the paper, highlighting the challenging scenario for Brazil to resume its economic and social development agenda amid a complex and unstable international context.

Brazilian Trade Flows and the Growing Importance of China

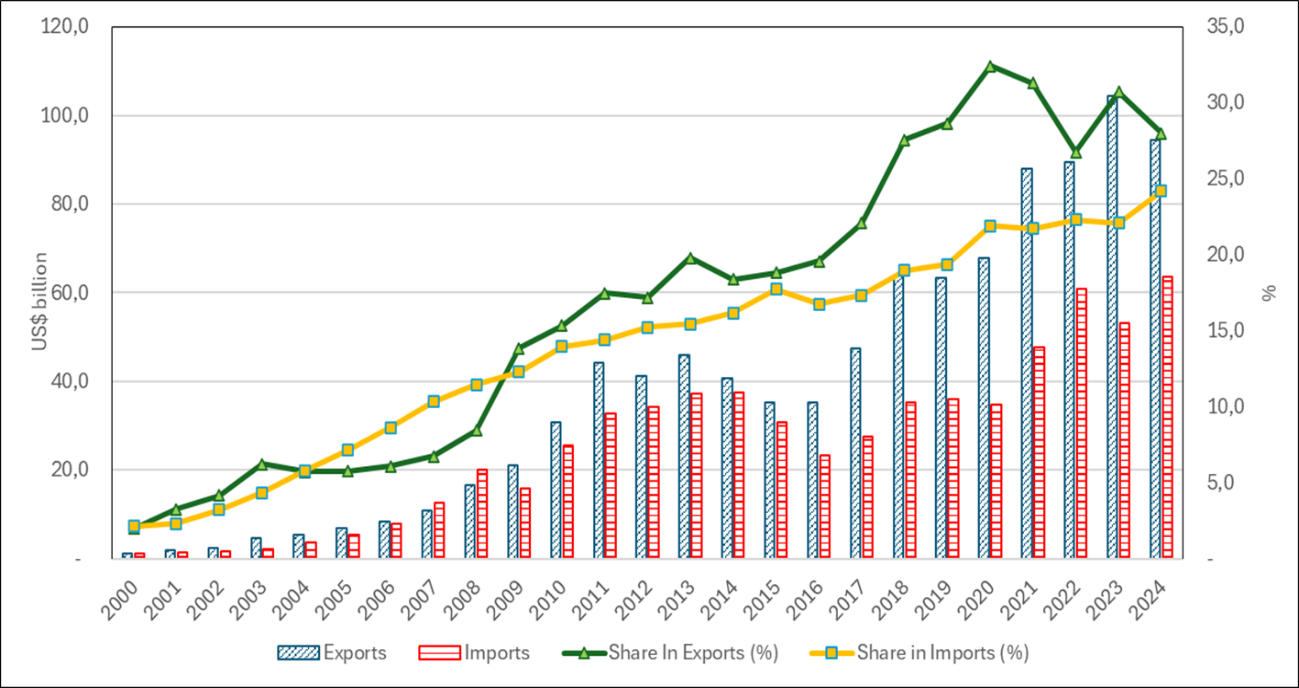

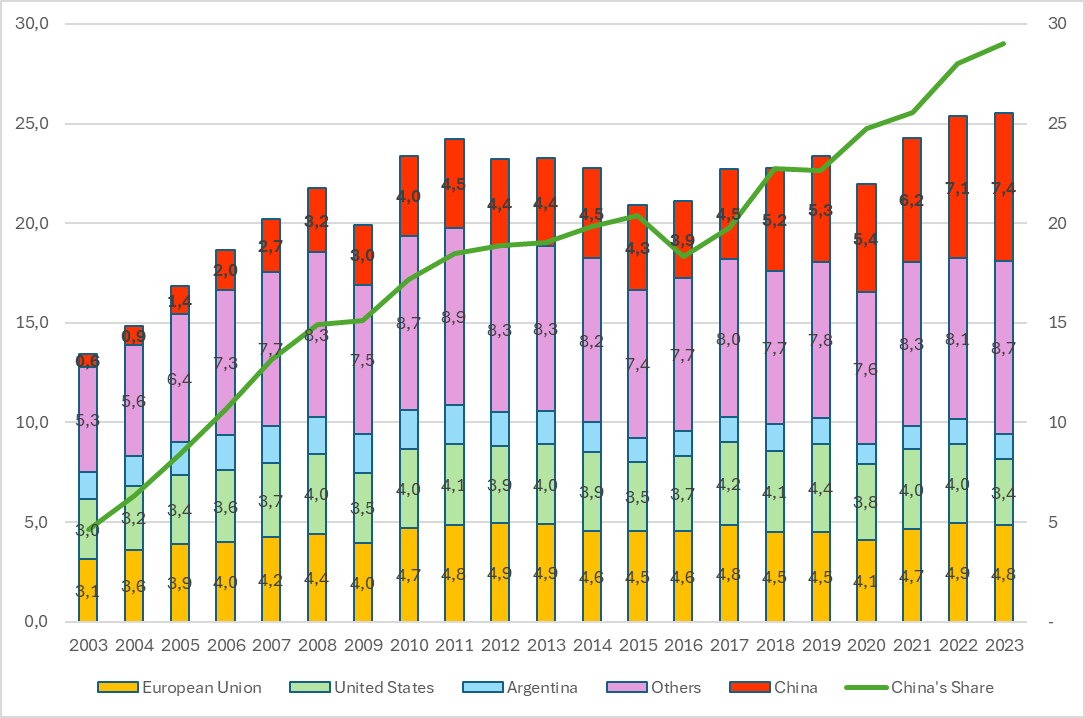

Since the beginning of the 21st century, trade relations between Brazil and China have experienced remarkable growth, culminating in the consolidation of China as Brazil’s main trading partner from 2009 onwards. In 2000, Brazilian exports to China amounted to approximately US$1 billion, reaching US$94 billion in 2024, thus surpassing the combined total of exports to the United States and the European Union. This figure represented about 28% of Brazil’s total exports. In the same period, imports from China totaled US$63 billion, corresponding to 24% of the country’s total imports. The trade surplus in Brazil’s favor with China, US$30 billion in 2024, accounted for approximately 41% of Brazil’s overall trade surplus.

Figure 1 – Foreign trade between Brazil and China. In value (US billions) and share of the total (%): 2000-2024

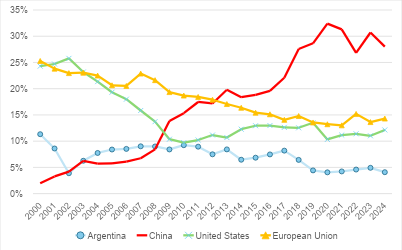

Figures 2 and 3 illustrate how the growth in China’s importance as Brazil’s trading partner has displaced other traditional partners. Regarding exports, the United States, which accounted for 25% of Brazilian exports in 2000, fell to 10% in 2009, regained some share thereafter, but reached only 12% in 2024. Brazil’s exports to the European Union also followed a downward trend, less pronounced than that of the United States between 2000 and 2010, but continued to decline until 2021, when they reached 13% of the total. From then on, the share stabilized and reached 14% in 2024. Finally, another traditional Brazilian partner, Argentina, showed an upward trend between 2002 and 2010, reaching 9% of Brazilian exports, but from that point on also lost share, reaching 4% in 2024.

Figure 2 – Share of Brazilian exports by country/region (%): 2000-2024

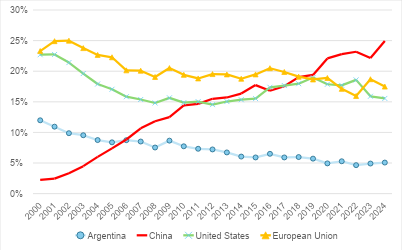

Figure 3 – Share of Brazilian imports by country/region (%): 2000-2024

With regard to imports, a similar trend was observed. While China showed continuous growth throughout the period, the share of Brazil’s other partners in imports declined significantly. It is noteworthy that, in this case, the United States recovered some share between 2013 and 2019, although from that point onward, a new downward trajectory was observed. In 2024, products from the United States accounted for 15% of Brazil’s total imports, about 11 percentage points lower than China. Imports from the European Union fell from 23% in 2000 to 17% in 2024. Argentina experienced one of the most significant reductions, as it accounted for 12% of Brazil’s purchases at the beginning of the period and only 5% in 2024.

Despite the extraordinary growth of trade relations with China, it is also important to highlight the marked asymmetry in the export and import profiles. Brazil’s surplus is largely the result of sales of primary products and resource-intensive manufactured goods, notably commodities such as oil, iron ore, and soybeans. More recently, there has also been an increase in exports of meat and pulp. On the other hand, Brazilian imports from China cover a wide range of manufactured products, from labor-intensive goods such as textiles and apparel to medium- and high-technology products like electronics and vehicles.

In the academic sphere, the high concentration of Brazil’s exports in natural resources to China has fueled intense debates. Terms such as “Dutch Disease,” “Resource Curse,” and “Core-Periphery Relationship” have been commonly used to highlight concerns about the trade profile with China (Jenkins, 2015; Powell, 2016; Borghi, 2020; De Assis and da Silva, 2020). A report published by UNCTAD (2021) indicates that the commodity dependence trap remains a problem affecting most developing countries, causing low growth, macroeconomic instability, and difficulties in diversifying the productive structure and increasing productivity. Shifting and diversifying the productive structure towards industrial and service sectors with greater incorporation of knowledge and technological content is seen as key to overcoming the commodity dependence trap. At the aggregate level, the effects of exchange rate overvaluation and the relative profitability of industrial activities are the most highlighted issues, which hinder this transformation (Nassif et al., 2017).

Concern over the high concentration of exports and the need to diversify Brazil’s exports to China has been compounded by environmental concerns, given the predominance of commodities with high potential for negative environmental impacts. The main concern has been deforestation resulting from the expansion of soy and livestock production in important biomes such as the Amazon and Cerrado (Fearnside and Figueiredo, 2015; Studart and Myers, 2021; Wilkinson et al., 2022). According to analysis by CDP (2019), driven by the growth in global protein demand, soybean production in Brazil increased by 66% between 2010 and 2017. From 2010 to 2016, this increase led to an additional 104 million tons of CO2 emissions as a result of deforestation and conversion of native vegetation. The report also estimated that in 2017, China’s soybean imports were associated with 6.5 million tons of CO2 emissions related to deforestation for soybean expansion in the Brazilian Amazon and Cerrado.

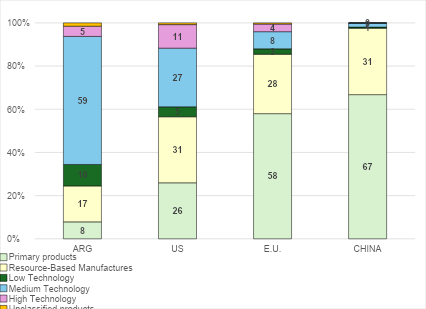

It is important to note that the export profile to China is more specialized, with a higher concentration of primary products and resource-intensive manufactures than with other major partners. Using the product classification by technological intensity developed by Lall (2000), it is evident that in 2024, these two groups (primary products and resource-intensive manufactures) accounted for 98% of Brazil’s total exports to China. Figure 4 shows how, in particular, the markets of Argentina and the United States have an export profile where medium- and high-technology manufactured products have greater relative importance. For Argentina, products classified as medium technology accounted for 59% of total exports to that country in 2024. For the United States, medium-technology products represented 27% of the export basket, while high-technology products accounted for 11% of the total. Exports to the European Union follow a pattern more similar to exports to China, although with a lower degree of concentration in primary and resource-intensive products. These two groups together accounted for 85% of the total in 2024.

Figure 4 – Exports to China by technology category and country/region (%): 2024

On the other hand, Brazil’s imports from China have a similar profile to those from the United States and the European Union, including a highly diversified set of manufactured goods, from labor-intensive to technology-intensive products. However, the volume of such imports from China is substantially higher.

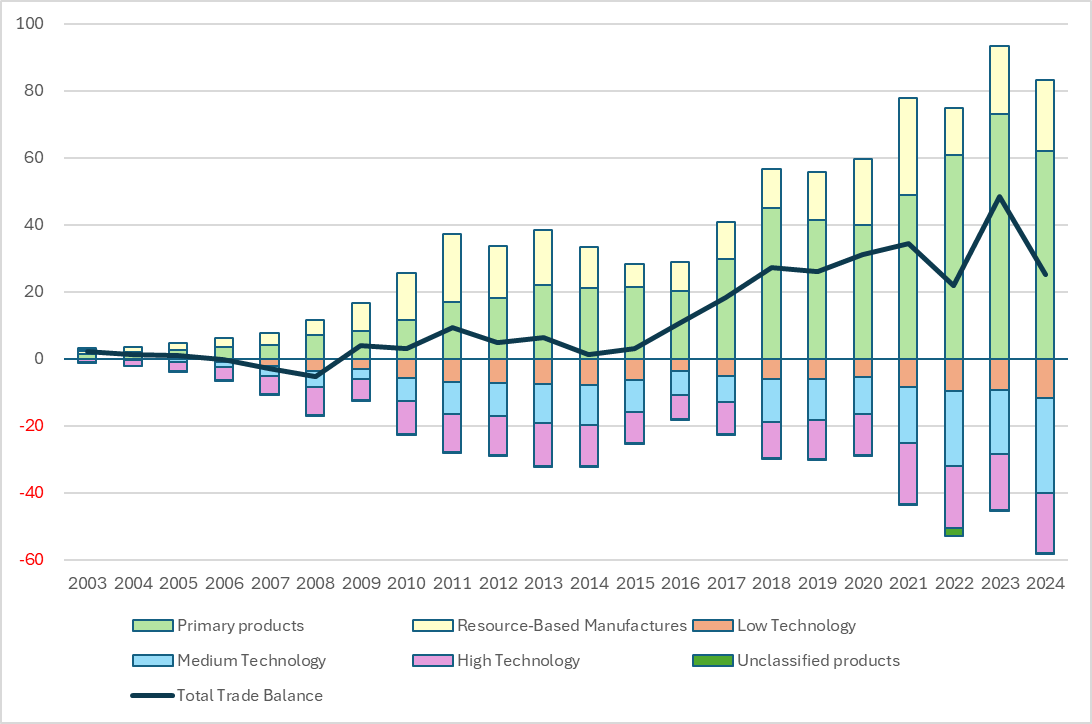

The difference observed in the profiles of export and import flows with China can be seen in Figure 5, through the bilateral trade balance, which has remained favorable to Brazil over time. However, this difference is the result of positive balances obtained with primary products and resource-intensive manufactures, especially food-related products. Conversely, in manufactured products, there is a large trade deficit, concentrated in high-technology products (mainly electronics) and medium-technology manufactures (machinery and equipment, automobiles, auto parts, chemicals, among others), but also in labor-intensive products (textiles, apparel, and footwear).

Figure 5 – Trade balance between Brazil and China by technology category (billion USD): 2003-2024

Notes: Billions USD in current prices.

Furthermore, the increase of Chinese imports in the domestic market is intertwined with the debate on deindustrialization due to competition effects with domestic industrial production.

Sugimoto and Diegues (2022) and Almeida et al. (2022) use the World Input-Output Database (WIOD) to highlight how, between 2000 and 2014, the dependence of Brazil’s manufacturing industry on inputs produced in China increased, to the detriment of domestic inputs. Almeida et al. (2022) emphasize that the effect of stimulating intra-sectoral activity in Brazil was, over time, displaced by the effect of stimulating Chinese productive sectors.

An indicator that can compare China’s effect with other countries is the import coefficient by origin. This indicator shows, out of the total domestic consumption of manufacturing activities, what percentage is supplied by imports from different sources. Between 2003 and 2011, there was a significant increase in Brazil’s import coefficient, mainly driven by exchange rate appreciation resulting from the commodities boom. In this interval, the national import coefficient rose from approximately 13% to 24%. Specifically, regarding China, this indicator increased from 0.6% to 4.5%. Although imports from other regions also grew, the pace of China’s advance was considerably faster, leading China to account for 18% of the total index in 2011.

In the subsequent period, marked by the turbulence of the global financial crisis and the slowdown of Brazilian economic growth from 2014 onwards, the aggregate import index stabilized. However, imports from China remained dynamic, while other international suppliers to Brazil stagnated or slightly contracted. From 2016, an increase in China’s share of the total is evident. In 2023, the overall coefficient reached 25%, with Chinese imports representing 7.4%, corresponding to 29% of the total. The coefficient related to imports from the United States has hovered around 4% since 2010. In 2023, it dropped more sharply to 3.4% of the total. For the European Union, the coefficient has oscillated around 4.7%.

Figure 6 – Import coefficient for the manufacturing industry by country of origin, percentage share: 2003-2023

It is clear, therefore, that in addition to supplying inputs and displacing other traditional suppliers, the growth of Chinese imports also reduced the share of domestic production supplying internal consumption over the period analyzed.

Finally, it is worth highlighting the effect on external markets for Brazilian industrial production. Notably, regional markets, especially Latin American and Mercosur countries, have always had an export profile dominated by manufactured products compared to other destination regions. Concern over the effects of Chinese competition in third markets in Latin American countries is recurrent and appears, for example, in Jenkins (2012), Bittencourt (2012), Jenkins and Dussel-Peters (2009), and Gallagher (2016).

Specifically for Brazil, Castilho et al. (2019) used the Constant Market Share methodology to estimate the losses and gains of different countries in the Latin American Integration Association (ALADI) manufactured goods markets, comparing Brazil and China. The data indicate that between 2000 and 2007, 43% of Brazil’s losses were associated with China’s gains, a figure that increased to 62% between 2007 and 2013. Not only did the percentage attributed to China increase, but the estimated value of losses rose from US$564 million to US$7.1 billion between the two periods. The most affected sectors were metal products, machinery and equipment, and transportation equipment.

Hiratuka (2016) used the same methodology and found that from 2001 to 2014, losses attributed to China accounted for 62% of Brazil’s total market losses in Mercosur, with a value equivalent to US$4.6 billion. Thus, China’s emergence exposed the insufficient progress in establishing a regulatory and institutional framework within Mercosur. Important opportunities for regional trade were missed; that is, the increase in imports from countries outside the bloc, with China’s growing prominence, occurred to the detriment of the market share of regional partners’ exports.

The difficulties associated with deindustrialization and the lack of competitiveness in Brazil’s industrial products have diverse and complex causes and cannot be attributed solely to Chinese competition. However, competition with China has made explicit the problems related to deindustrialization and the structural change needed to increase productivity and income levels in the country, even though it supported growth in exports and trade surpluses. The next section addresses the investment flows of Chinese companies in Brazil.

Foreign Direct Investment, the Role of China, and New Areas of Competition

The internationalization process of Brazil’s productive structure is quite old. In fact, the very formation of the Brazilian industry in the postwar period was associated with the establishment of a tripartite “division of labor,” in which foreign-capital companies were responsible for technology- and capital-intensive stages, such as in the automotive sector, while state-owned enterprises assumed basic input sectors intensive in capital, like the steel, petrochemical, and oil industries. Domestic capital, in turn, focused on light industry and some supplier branches of industries dominated by foreign capital, such as the auto parts sector. In this phase of Brazilian industrialization, which covers the postwar period up to the 1980s, companies from the United States and Europe were the major foreign investors in Brazil. Among Asian firms, Japanese companies also established important bases in Brazil, especially from the 1970s onward, while South Korean companies began to set up operations in the country in the 1990s.

It is reasonable to state that Brazil has always built its productive structure with a strong presence of foreign companies. Throughout the 1990s privatization process, foreign presence increased even further, while maintaining the predominance of companies from the United States and Europe, with Japan and South Korea occupying a somewhat less important position.

The 2000s saw the growth of Chinese investments. In fact, the importance of the Chinese presence is a phenomenon observed in Brazil especially from the second decade of the century.

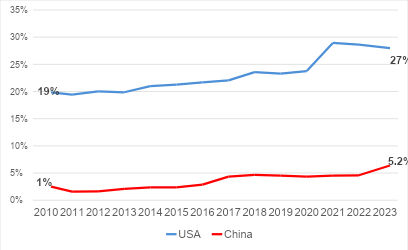

Considering the stock of FDI data from the Central Bank of Brazil and accounting for the ultimate controlling investor – thus avoiding distortions from considering the immediate investor, which is often inflated by the participation of tax havens such as the Cayman Islands – it is evident that China represented only 1% of total FDI stock in 2010, rising to just over 5% in 2023 (Figure 7).

Figure 7 – Share of China and the United States in the Stock of Foreign Direct Investment, percentage share: 2010-2023

Although China has surpassed the United States as Brazil’s main trading partner, the direct investment gap remains substantial. As highlighted, US companies have been present in Brazil since the early 20th century and, especially after World War II, consolidated their presence in various industrial and service sectors, particularly in knowledge- and technology-intensive segments.

This difference persists, despite Chinese growth, also due to the increased participation of the United States in the recent period, as shown in Figure 7. In 2023, capital from the United States accounted for 27% of total investment in Brazil.

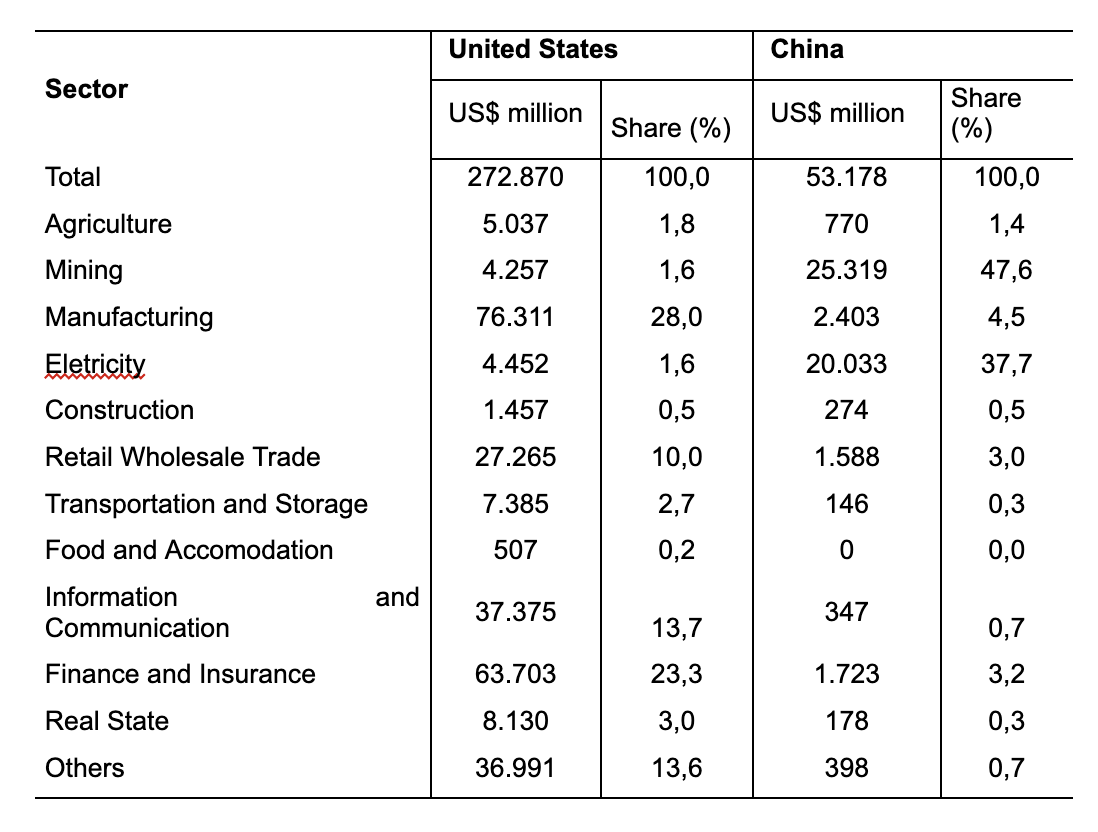

The discrepancy is also evident in the sectoral profile of investments (Table 1), with US presence being much more significant in manufacturing, as well as in financial services and information technology. Chinese investments, on the other hand, have been more concentrated in mineral extraction and the electric power sector. Schutte and Debone (2017), Barbosa (2020), and Ramos et al. (2022) emphasize how, in a short period, Chinese companies have become highly relevant players in the generation, transmission, and distribution of electricity in Brazil. Although the extractive and oil sectors lost importance between 2010 and 2019, they remained very important, with a share slightly higher than that of electricity and water.

Table 1 – Foreign investment stock in Brazil by sector: China vs. the United States (million USD and % share). 2023.

It is important to note, however, relevant changes that have been occurring in the more recent period, largely associated with the new profile of Chinese development, which prioritizes innovation and the formation of new quality productive forces. China’s technological development, as well as its expansion into sectors such as telecommunications, digital technologies, artificial intelligence, electric vehicles, and renewable energy, are central to this strategy. In 2022, investments in these sectors accounted for 58% of total Chinese direct investment in Latin America and the Caribbean (Myers, 2024).

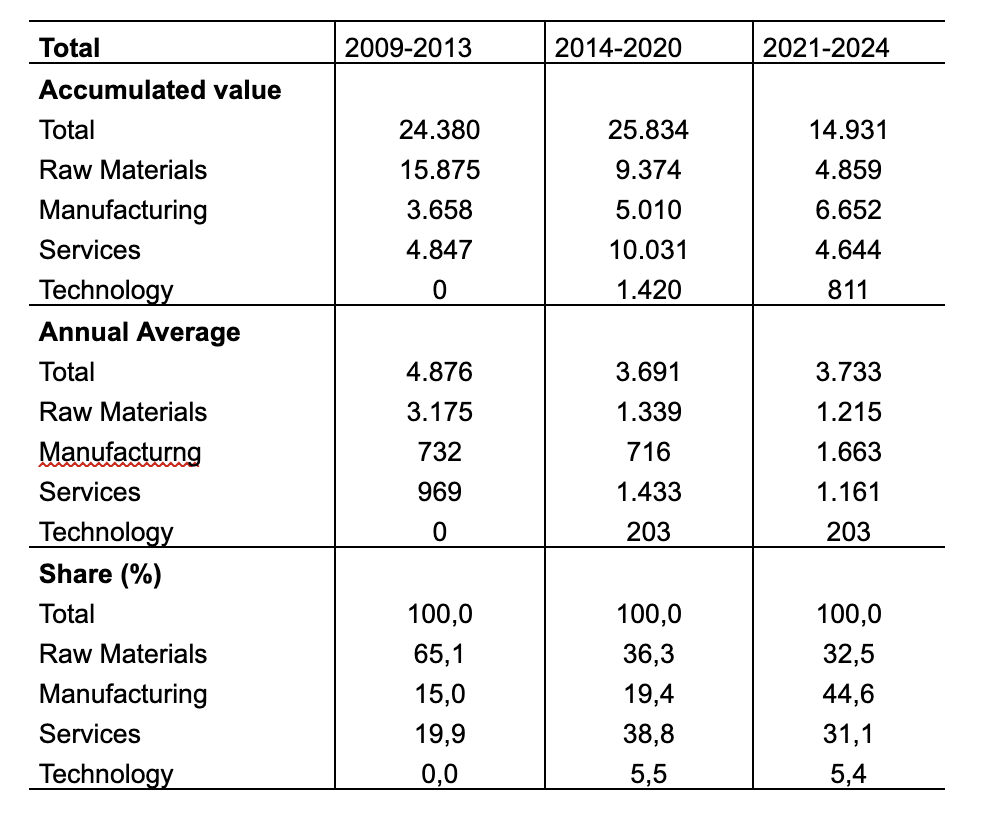

In the Brazilian case, this shift is also noticeable. Considering investment flows according to information from the Overseas Foreign Direct Investment (OFDI) Monitor organized by the ALC-China Network, three phases can be distinguished for the period 2009-2024. In the first (2009 to 2013), investments in raw materials prevailed, with sectors such as oil and iron ore drawing great interest from Chinese companies in Brazil. Between 2014 and 2020, investments in raw materials shared prominence with services, especially in the area of electric power. From 2021 onward, manufacturing industries became a key target. Whether in terms of resource volume or relative participation, the increase in Chinese investments in the manufacturing sector is evident (Table 2).

These investments have reached significant sectors, such as automobile production by companies like BYD and GWM, with the automotive sector being emblematic of these recent transformations. The automotive sector is one of the main industrial segments in Brazil. In 2024, national production reached 2.3 million vehicles, positioning the country as the sixth largest consumer market and the eighth largest producer worldwide.

GWM entered the Brazilian market in 2021 with the acquisition of the Mercedes-Benz plant, which had ceased car production in the country in 2020. In 2022, the company announced investments of around US$ 730 million through 2025, followed by an additional US$ 1.1 billion in 2025 for the period 2026 to 2032, expanding the plant’s production capacity from 20,000 to 50,000 vehicles.

Table 2 – Chinese investments in Brazil by major sector (million USD)

BYD, in turn, has been present in Brazil since 2015, manufacturing solar panels and electric bus chassis. The company substantially increased its investments by acquiring the former Ford factory in Camaçari, Bahia, which had ceased operations in 2021 and was returned to the Bahia state government in 2023, allowing BYD to take over the plant with an investment of about US$ 50 million. After the acquisition, the company announced US$ 550 million to implement local production and modernize facilities to reach an installed capacity of 150,000 vehicles per year. Companies like BYD, Great Wall Motors, and Chery stand out as the main drivers of the increase in electrified vehicle volumes in Brazil.

It is important to emphasize that the entry of Chinese companies occurred with plug-in hybrid (PHEV) and battery electric vehicles (BEV), rapidly increasing the diffusion of electric vehicles in the Brazilian market. Electrified vehicles accounted for only 1% of the market in 2020, reaching 7% in 2024. This expansion resulted largely from the establishment of distribution networks and an initial increase in imports. 2023 and 2024 showed significant growth in imports relative to sales and local production. At the same time, companies have announced investments in domestic production.

This sector is a priority in Brazil’s new industrial policy. Specifically, the policy for the sector is called the Green Mobility and Innovation Program (Mover), announced at the end of 2023, which reinforces incentives for R&D projects and decarbonization. The program provides, for example, increased financial incentives for investments in research and development, according to the degree of production localization, the expansion and diversification of exports, and the incorporation of sustainable technologies.

The government also announced a gradual increase in import tariffs for electrified vehicles between 2024 and 2026. The tariff for battery electric vehicles increased to 10% in January 2024, 18% in July 2024, 25% in July 2025, and will reach 35% in July 2026. This measure aims to stimulate domestic production, promoting greater alignment between the strategies of Chinese companies and efforts for reindustrialization and strengthening of national production chains.

Both companies are still operating (as of early 2026) mainly with imported CKD (Completely Knocked Down) kits but plan to progressively increase the localization of components and are negotiating with local auto parts suppliers. GWM and Bosch, for example, are negotiating to develop flex-fuel engines for hybrid vehicles.

This movement by Chinese companies has provoked a strong reaction from companies historically established in the Brazilian automotive sector, such as Volkswagen, Stellantis, General Motors, and Renault. Until recently, these companies had been betting on the development of mild and conventional flex-fuel hybrids. This technology, developed in Brazil in the early 2000s, allows vehicles to use any gasoline-ethanol blend, thus reducing CO2 emissions compared to pure gasoline use. Moreover, gasoline used in Brazil normally contains a blend currently at 30% ethanol.

However, the entry of Chinese companies’ competition in the market has forced these firms to accelerate their electrification strategies. Volkswagen, for example, has announced that all its models in Brazil will feature some form of electrification.

More commonly, however, they have turned to new or existing partnerships with Chinese companies to accelerate and complete their electrified vehicle portfolios.

Stellantis became a shareholder in the Chinese company Leapmotor, founded in 2015, in 2023. In 2025, it announced a strategy to expand the Leapmotor brand beyond China and launched it in Brazil, using Stellantis’s dealership network and infrastructure to sell electric cars. In November 2025, Stellantis confirmed that Leapmotor vehicles would be produced in Brazil starting in 2026. The new Chinese brand, which will enter the Brazilian market with a fully electrified lineup, will be produced at the Goiana Automotive Hub in Pernambuco.

GM is adopting a similar strategy in Brazil. On the one hand, the company is accelerating the launch of flex-fuel hybrid products. On the other, GM announced in 2025 that it will assemble an electric vehicle developed by Wuling, a joint venture between GM and SAIC in China. The Chevrolet Spark EV will be assembled in SKD (Semi Knocked Down) mode at the former Ford/Troller plant in Horizonte (CE).

Finally, it is worth highlighting the agreement between Renault and Geely for a strategic partnership in Brazil. Geely acquired 26% of Renault do Brasil, guaranteeing access to the Brazilian plant to produce Geely-branded vehicles. Additionally, investments of R$ 3.8 billion were announced for adjustments, including stamping, bodywork, and painting stages, to enable full-scale production at the São José dos Pinhais (PR) facility, focusing on hybrid and electric models. The strategy allows Renault to incorporate electrified vehicles into its portfolio, while for Geely, it represents a rapid entry into Brazilian production without the longer period of investment and modernization seen at GWM and BYD plants.

Conclusion

Brazil’s economic relations with China are undergoing significant changes. The main drivers of this transformation appear to be associated with the impacts of China’s new development strategy, which is centred on activities with higher technological intensity.

In this context we see both the pursuit to access markets with more sophisticated products and, in the early stages of production chains, strategies to secure critical resources for China’s technological advancement. In other South American countries, such as Chile, Bolivia, and Argentina, China has made significant investments to secure critical minerals such as lithium and copper.

However, in Brazil, given its more diversified productive structure, this dynamic may create opportunities for greater productive complementarity in strategic industrial chains, especially those aligned with the priorities of the new Brazilian industrial policy.

The shift in Chinese investment profiles, as evidenced by the pursuit of foreign markets in sectors where the Chinese domestic market has already reached a high degree of maturity, is a recent transformation and is likely to provoke significant changes in the Brazilian economic landscape, as seen in the profile of Chinese investments in the Brazilian automotive sector. These investments can yield positive outcomes if they increase productivity, productive modernisation, and higher productive and technological content carried out within Brazilian territory. The new wave of investments is still at an early stage and needs to be monitored to assess its actual results. For example, manufacturing plants in the automotive sector only began production in the second half of 2025 and are in the process of increasing local production content, making it impossible to draw conclusive assessments about their impacts. It is, however, clear that this could generate significant changes in relation to the pattern established thus far in the export of raw materials and the import of technology-intensive manufactured goods.

It is likely that the interest of Chinese companies in other growing markets in Brazil will further intensify competition with American and European companies in more knowledge-intensive sectors, such as data centres, information technology services, pharmaceuticals, and biotechnology. Some stages of the production chains in these sectors, such as the extraction of critical minerals and rare earths, are considered strategic by both China and the United States.

These factors become more relevant considering that the United States’ lack of interest in South America since the failure of the FTAA negotiations is giving way to a renewed willingness to regain influence in the region and intensify the strategic dispute with China. From direct interference in Venezuela to speculation about a free trade agreement with Argentina, it is evident that the attention devoted to the region’s economies is likely to be substantially greater than in the past.

The imposition of 50% import tariffs on Brazil in June 2025, even considering the relaxation with the removal of several products from the list of surcharged items in November of the same year, shows that there are still pressures that may affect Brazil. Access to critical minerals and rare earths may be among the United States’ interests in granting new trade benefits.

Furthermore, the intensification of the geopolitical dispute between China and the US challenges Brazil to define an autonomous strategy capable of seizing the opportunities created by this competition, without becoming excessively dependent on either power. This requires an active industrial policy, diplomatic coordination, and mechanisms to protect national strategic sectors, ensuring that technological and productive development is geared towards reducing inequalities and achieving sustainable growth.

In this context, Brazil faces complex challenges to guide this increased international competition towards tangible benefits for its economic development. One of the main obstacles is the need to strengthen its capacity for more qualified integration into global value chains, moving beyond the mere export of commodities and raw materials. To this end, it is essential to invest in innovation, education, and technological infrastructure to create a supportive environment for high value-added sectors.

Another relevant challenge concerns the governance of strategic natural resources, such as critical minerals and rare earths. The growing international demand for these inputs may lead to pressures for accelerated exploitation, with potential environmental and social impacts. Thus, Brazil needs to balance the interests of attracting foreign investment with the implementation of robust sustainability policies and local value addition, avoiding the simple re-primarization of its economy.

Nevertheless, there is also a scenario of intensifying tensions in bilateral negotiations with the United States. Simultaneously, Chinese economic interest – whether in the market for sophisticated products and services or in critical minerals – is likely to remain. Such a situation will require Brazil to make a substantially greater effort than in the past to balance between these two major players, pursuing its own interests and developing strategies capable of overcoming the traditional challenges of low growth and inequality, as well as addressing new problems related to environmental issues.

References

ABDENUR, A. E.; SANTORO, M. e FOLLY, M. What Railway Deals Taught Chinese and Brazilians in the Amazon. Carnegie Endowment for International Peace, 2021.https://carnegieendowment.org/files/Abdenur_et._al_China_Brazil_REVISED.pdf

ALMEIDA, L. M. L.; PIRES, P.; LEITE, A. C. C. Relações comerciais com a China e a desindustrialização brasileira entre 2000 e 2014. um estudo baseado na análise inter-regional do insumo-produto. Revista da SEP, n. 63, mai-ago, p. 95-126, 2022.

BANCO CENTRAL DO BRASIL. Relatório de Investimento Direto. Brasília: BCB, 2024.

BARBOSA, P. H. B. New Kids on The Block: China’s Arrival in Brazil’s Electric Sector. Boston University Global Development Policy Center, December, 2020. https://www.bu.edu/gdp/files/2020/12/GCI_WP_012_Pedro_Henrique_Batista_Barbosa.pdf

BORGHI, R. A. Z. China’s Trade Specialization pattern with Latina America and African Economies: Revisiting the Core-Periphery dichotomy. Revista Tempo do Mundo, vol 24, p. 27-52, 2020.

CABRÈ, M. M.; GALLAGHER, K.; LI, Z. Renewable Energy: The Trillion Dollar Opportunity for Chinese Overseas Investment. China & World Economy, Vol. 26, No. 6, p. 27-49, 2018.

CARIELLO, T. Investimentos Chineses no Brasil 2022. Tecnologia e Transição Energética. Rio de Janeiro, Conselho Empresarial Brasil China, 2023.

CASTILHO, M. DOS R.; COSTA, K. G. V. DA; TORRACCA, J. F. A importância do mercado Latino-Americano e da competição chinesa para o desempenho recente das exportações brasileiras de produtos manufaturados. Porto Alegre, Análise Econômica, vol. 37, n. 72, p. 7-38, 2019. https://doi.org/10.22456/2176-5456.68199

CDP. Decoupling China’s soy imports from deforestation driven carbon emissions in Brazil. Trase/CDP, 2019. https://cdn.sanity.io/files/n2jhvipv/production/e775177aa41eef52c3ddbaa4d177c49932675c59.pdf

CINTRA, M. A. M.; PINTO, E. C. China em transformação: transição e estratégias de desenvolvimento Revista de Economia Política, vol. 37, nº 2, p. 381-400, abril-junho/2017.

COSTA, A. And RICUPERO, R. Brasil e Estados Unidos na Era Trump 2.0. O Retorno ao Radar Diplomático. CEBRI. 2025.

DE ASSIS, R. J. S.; DA SILVA, O. F. A. A reprimarização no Brasil sob a ascensão da geopolítica chinesa no comércio exterior (2008-2018). Brazilian Journal of Development, v. 6, n. 3, p. 12121-12139, 2020.

DIEGUES, A. C.; ROSELINO, J. E. Industrial policy, techno-nationalism and Industry 4.0: China-USA technology war. Brazilian Journal of Political Economy, v. 43, p. 5-25, 2023.

DINLERSOZ, E. M.; FU, Z. Infrastructure investment and growth in China: A quantitative assessment. Journal of Development Economics, vol 158, 2022. https://doi.org/10.1016/j.jdeveco.2022.102916

DITTMER, L. Xi Jinping’s “new normal”: Quo Vadis? Journal of Chinese Political Science, vol. 22, n. 3, p. 429-446, 2017. http://dx.doi.org/ 10.1007/s11366-017-9489-4

DUSSEL PETERS, E. Security-shoring y la nueva relación económica triangular China- Estados Unidos-México,” Revista de Economía Mexicana. Anuario UNAM, no. 9 .p. 157-188. 2024.

DUSSEL PETERS, E. Latin America, China and Great Power Competition. New Triangular Relationships. Boulder, CO: Lynne Rienner Publishers, 2025.

FAROOKI, M.; KAPLINSKY, R. The Impact of China on Global Commodity Prices. New York: Routledge, 2012

FEARNSIDE, P. M.; FIGUEIREDO, A. M. R. China’s Influence on Deforestation in Brazilian Amazonia: A Growing Force in the State of Mato Grosso. Boston University Global Governance Initiative Discussion Paper, 2015-3, 2015.

GALLAGHER, K. The China triangle. Nova York: Oxford University Press, 2016.

GLAESER, E. HUANG, W. MA, Y e SHLEIFER, A. A real estate boom with Chinese characteristics. Journal of Economic Perspectives, vol. 31, n. 1, p. 93-116, 2017.

HEINE, J. América Latina: o não alinhamento ativo e a disputa entre os Estados Unidos e a China. Conexão América Lativa, ano 4, volume 2. São Paulo: Edições Plataforma Democrática, 2025.

HIRATUKA, C. Chinese OFDI in Brazil. In: DUSSEL PETERS, E. (Org.). China’s Foreign Direct Investment in Latin America and the Caribbean. Conditions and challenges. Cidade do México: Universidade Autonoma de México. 2019.

HIRATUKA, C. Changes in the Chinese Development Strategy after the global Crisis and its impacts in Latin America. Rio de Janeiro, Revista de Economia Contemporânea. vol. 22, n. 1, p. 1-25, 2018.

HIRATUKA, C. Impactos de China sobre el proceso de integración regional de Mercosur. In Dussel Peters, E. (ed) La Nueba relacion Comercial de America Latina y el Caribe con China. Integración o desitegración regional? Cidade do México: Unión de Universidades de América Latina y el Caribe, 2016.

HIRATUKA, C. Why Brazil Sought Chinese Investments to Diversify Its Manufacturing Economy. Carnegie Endowment for International Peace. Octobre, 2022.

JACKSON, M. M.; LEWIS, J. I; ZHANG, X. A green expansion: China's role in the global deployment and transfer of solar photovoltaic technology. Energy for Sustainable Development, Volume 60, p. 90-101, 2021.

JAGUARIBE, ANNA. (org). Direction of Chinese global investments: implications for Brazil. Brasília : FUNAG, 2018.

JENKINS, R. Is Chinese competition causing deindustrialization in Brazil? Latin American Perspectives, v. 42, n. 6, p. 42-63, 2015.

JENKINS, R. Latin America and China: a new dependency? Third World Quarterly, vol. 33, n. 7, p. 1337-1358, 2012.

JENKINS, R.; PETERS, E. D. (Orgs.) China and Latin America: economic relations in the twenty-first century. Bonn: German Development Institute, 2009.

KUPFER, DAVI; ROCHA, FELIPE. F. Direções do investimento chinês no Brasil 2010-2016:estratégia nacional ou busca de oportunidades. In JAGUARIBE, ANNA. (org). Direction of Chinese global investments: implications for Brazil. Brasília: FUNAG. 2018.

KWUAN, C. H. The China-US Trade War: Deep-Rooted Causes, Shifting Focus and Uncertain Prospects. Asian Economic Policy Review, Vol. 15, p. 55-72. 2020.

MEDEIROS, C.A; TREBAT, N. M. From Complementarity to Rivalry: The Political Economy of US-China Relations. ASSA Annual Meeting. San Antonio, 2024.

MYERS, M., AND K. GALLAGHER. Chinese Finance to LAC in 2016. The Dialogue. 2017. https://www.bu.edu/gdp/files/2017/11/Chinese-Financeto-LAC-in-2016-Web-and-email-res.pdf

MYERS, M., MELGUIZO, A. AND WANG, Y. “New Infrastructure”. Emerging Trends in Chinese Foreign Direct Investment in Latin America and the Caribbean. The Dialogue Leadership for the Americas. China LAC report, 2024. https://www.thedialogue.org/wp-content/uploads/2024/01/Emerging-Trends-in-Chinese-Foreign-Direct-Investment-in-LAC.pdf

NASSIF, A.; CASTILHO, M. R. Trade patterns in a globalised world: Brazil as a case of regressive specialisation, Cambridge Journal of Economics, Volume 44, Issue 3, May 2020, Pages 671-701, https://doi.org/10.1093/cje/bez069

NAUGHTON, B. The rise of China’s Industrial Policy, 1978-2020. Cidade do México: UNAM, 2021.

OLIVEIRA. G. L. T. AND MYERS, M. The Tenuous Co-Production of China’s Belt and Road Initiative in Brazil and Latin America. Journal of Contemporary China, Vol 30, n. 129. P. 481-499, 2020. DOI: 10.1080/10670564.2020.1827358.

POWELL, D. China-Brazil Economic Relations: Too Big to Fail? In Margaret Myers and Carol Wise (Ed). The political economy of China-Latin American relations in the new millennium : brave new world. New York, NY : Routledge, 2016.

RAMOS, D., LESSA, A.C., SILVEIRA, L.U. One Step Closer: The Politics and the Economics of China’s Strategy in Brazil and the Case of the Electric Power Sector. In: BERNAL-MEZA, R., XING, L. (eds) China-Latin America Relations in the 21st Century. Londres: International Political Economy Series, Palgrave Macmillan, 2020. https://doi.org/10.1007/978-3-030-35614-9_3

RAMOS. D. S. MACEDO. B. V. Chinese multinational corporations in Brazil: strategies and implications in energy and telecom sectors. Revista Brasileira de Política Internacional, vol. 57, n. 1, p. 143-161, 2014.

ROSITO, T. Bases para uma estratégia de longo prazo do Brasil para a China. Rio de Janeiro: Conselho Empresarial Brasil China, 2020.

SCHUTTE, G. R. Oásis para o capital. Curitiba, Apris Editora, 2020.

SCHUTTE, G. R, E DEBONE. V. S. A expansão dos investimentos diretos Chineses. O caso do setor de energético Brasileiro. Conjuntura Austral, vol.8, n.44, p.90-113, 2017.

SHEKHAR, A.; PRESBITERO, A. AND RUTA, M. Geoeconomic Fragmentation: The Economic Risks From a Fractured World Economy. CEPR Press, 2023.

STUDART, R.; MYERS, M. Reimagining China-Brazil Relations Under the BRI: The Climate Imperative. CFR/CEBRI, 2021. https://cdn.cfr.org/sites/default/files/pdf/studart-myers-cfr-cebri-paper_0.pdf

SUGIMOTO, T. N.; DIEGUES, A. C. A China e a desindustrialização brasileira: um olhar para além da especialização regressiva. Nova Economia, v. 32, p. 477-504, 2022.

TEIXEIRA, I.; ROSSI, T. Brasil e China: Elementos para a Cooperação em Meio Ambiente. Cebri Policy Paper, 2020. https://www.cebri.org/media/documentos/arquivos/Relatorio_A4_PT_6jul-compactad.pdf.

UNCTAD. World Investment Report. International Production Beyond the Pandemic. Geneva: UNCTAD, 2020.

UNCTAD. Escaping from the Commodity Dependence Trap through Technology and Innovation. Commodities & Development Report 2021. Geneva: UNCTAD, 2021.

UNIDO. Industrial Development Report 2020: Industrializing in the digital age. Viena: UNIDO, 2019.

WILKINSON, J., ESCHER, F. GARCIA, A. The Brazil-China Nexus in Agrofood: What Is at Stake in the Future of the Animal Protein Sector. International Quartely for Asean Studies. Vol. 53, p. 251-277, 2022.